| The Bullroarer - Tuesday 6th May 2008 | The Oil Drum: Australia/New Zealand | The Bullroarer - Thursday 8th May 2008 |

$100 a barrel: Going, Going....

Posted by aeldric on May 6, 2008 - 7:00pm in The Oil Drum: Australia/New Zealand

This is a guest post by Phoenix, an engineer working in the energy sector, and a friend of mine for well over 3 decades.

In January 2006 Phoenix emailed me a spreadsheet that predicted an oil price of $100/barrel by 2008, followed by an ongoing geometric rise in oil prices. I remember immediately phoning him to point out that the scenario was impossible because it is unsustainable - $100/barrel would cause economic havoc comparable to the oil shock of the 1970s and if a geometric price progression followed, then no economic recovery would be possible and... well, I recall using the phrase “rioting in the streets inside of 18 months”.

As we know, oil hit $100 in January 2008 and kept climbing, surpassing even Phoenix’s predictions. So when Phoenix offered to explain the model that generated those numbers, I leapt at the opportunity. Here is the story of how Phoenix became Peak Oil aware and generated his Price Calculator.

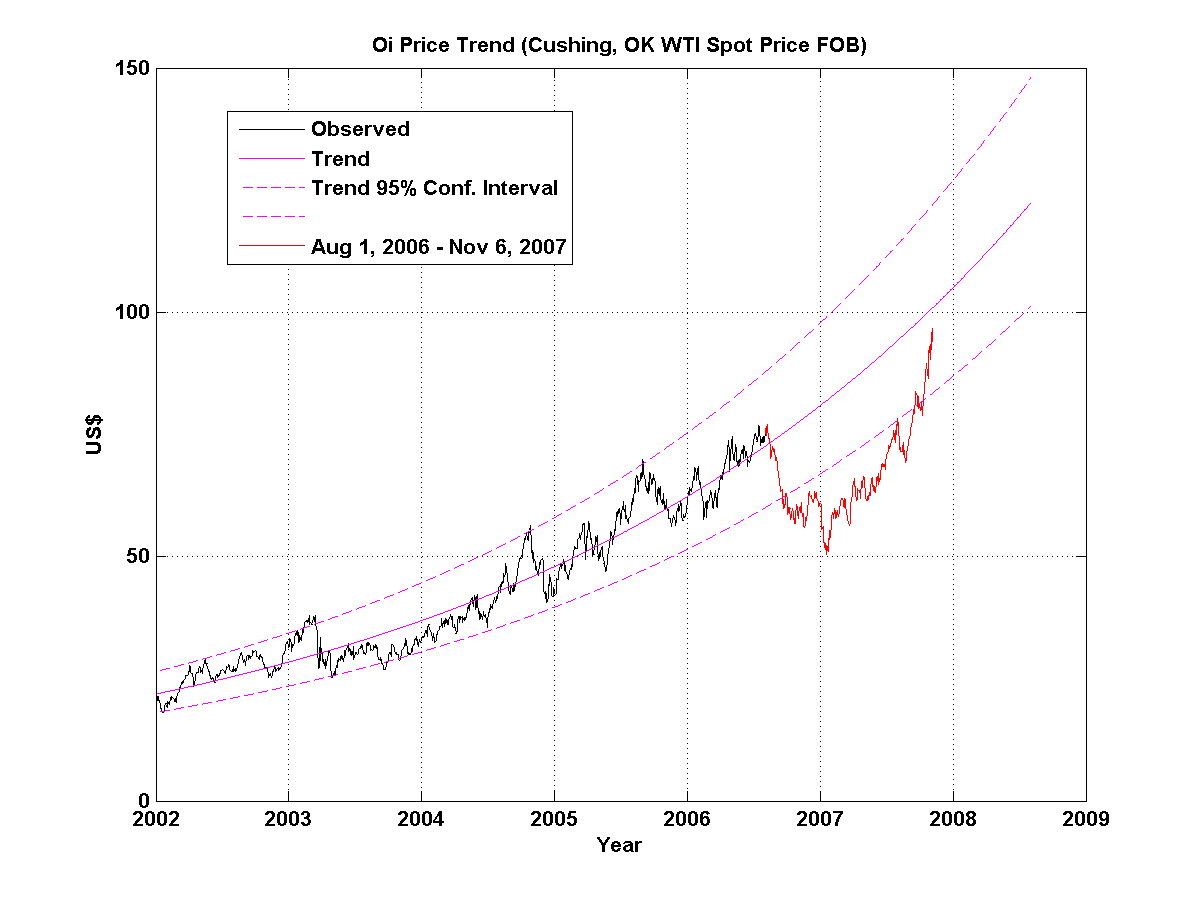

Click to Enlarge

Going, Going .... Gone

So what’s a barrel of oil really worth?

At the start of 2006 I became peak oil aware. Most of the readers of TOD will have lived through the turmoil of concern and dismay that this realisation usually brings on. In the months following, I proceeded to digest as much information on the topic as I could. However, after a time I noted that, while there was an abundance of predictions on amounts of oil and the depletion rates, there was little in the way of forecasts as to the future oil prices that would result.

At that time (and still today) I was an avid believer that the consequences of oil depletion will unfold as an economic crisis rather than as direct impacts from the shortage of energy. This being the case then why was there virtually no debate or a plethora of predictions as to the long range prices?

Perhaps everyone was relying on the output of the IEA for such forecasts? A quick review of the IEA numbers at the time was distressing. They were forecasting a drop in the price back to the US$40-$50 range. Even worse, world governments were probably using these predictions to set energy, social and infrastructure policy. I decided for my own piece of mind, to attempt to generate a simple model for predicting the long range oil price.

Basic Theory

Traditional oil market economic theory seems to be modelled around the notion that the price for a commodity is simply a reflection of the input costs. Markets, while they may experience temporary upsets due to imbalance between supply and demand, through the forces of competition will correct themselves so that prices are governed by costs.

Being an engineer rather than an economist I felt at liberty to toss the above theory out the window. It seemed to me overly reliant on the concept that the world was infinite and that markets always have the capacity to expand to meet demand.

Instead I started from the premise that the production of a commodity is limited. Of all those people vying for the commodity someone inevitably will miss out. They will not be able or willing to pay the market price. The price then will be governed by the maximum amount that this person is prepared to pay.

Supply

The starting position for the model was the prediction of oil supply rates over the future 30 years. As mentioned above there are many, many predictions concerning these numbers. I had to select one based on a consensus of the data available. I used a simple bell curve with the following parameters:

- peak of 85 Mbpd in 2007

- ultimate remaining capacity 850 billion barrels

- standard deviation set to give a depletion rate of 2.7 % by 2020

I am sure there will be a range of views on the veracity of these numbers.

On top of this base supply number I had to account for the growth of alternative fuel substitutes that will inevitably develop as the oil price climbs to a point that makes them viable. Predicting the capacity and ultimately the take-up of these alternatives is a little tricky. I lumped these into two areas:

- Alternative fossil based fuels (Oils sands, Coal to Liquid and Gas to Liquids)

- Renewable fuels

Against each of these I assigned an estimated * maximum capacity that was achievable and a price sensitive take-up rate.

Demand

As indicated above my basic premise for the model was demand destruction due to price sensitivity. To facilitate this I divided the demand into a number of economically predictable groups. This division was somewhat compromised by the necessity to obtain current consumption rates for these groups. The first division was made between OECD and non OECD countries. Within this I divided into the following sectors:

- Personal Transport

- Public Transport

- Heating

- Industry

- Shipping

- Air Transport

- Military

- Power Generation

- Products

Even this list involved a degree of interpretation *of the available data on consumption.

Against each of these sectors I assigned * a price sensitivity profile. As far as I have been able to research there is no definitive numbers or reported figures for these profiles. In my research I have come across a number of reports that provide indications for particular national groups. Where possible I have ensured that the profiles I have used are consistent with these reports. For the most part, however, these numbers are based on my personal experience and the experience of some of my associates. This is not ideal but it is the best I could do.

Model

I constructed the model in spreadsheet form. It simply compares the demand and supply and determines the price level necessary to suppress the demand to meet the supply. I have set the model up on a yearly period going out to 2040.

Results

Having run the model for the last two years I have noted the following:

- The results while fairly accurate in emulating the observed market price for oil, do not take into account a number of distorting factors affecting the market. These factors include, supply disruptions and the human factors (greed and panic) that affect any market.

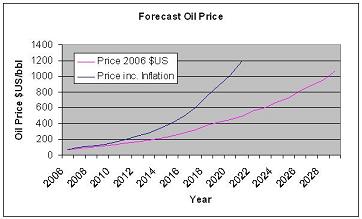

- The prices are on a 2006 USD basis. I subsequently added an allowance for inflation into the analysis. Anyone want to take a guess at what inflation will be in 30 years time? I have used a consumption- weighted figure between OECD and non-OECD current inflation rates and applied it to all future years.

- There will be an increasing trend for governments to hoard and lock up future supply. I have made a very rough attempt to * forecast the volume and timing of this factor in the spreadsheet. My view is that by 2030, all traditional oil sources will be subject to this government interference. Hence the above curve only represents the market price up till that time.

See the oil price prediction curve below:

Click to Enlarge

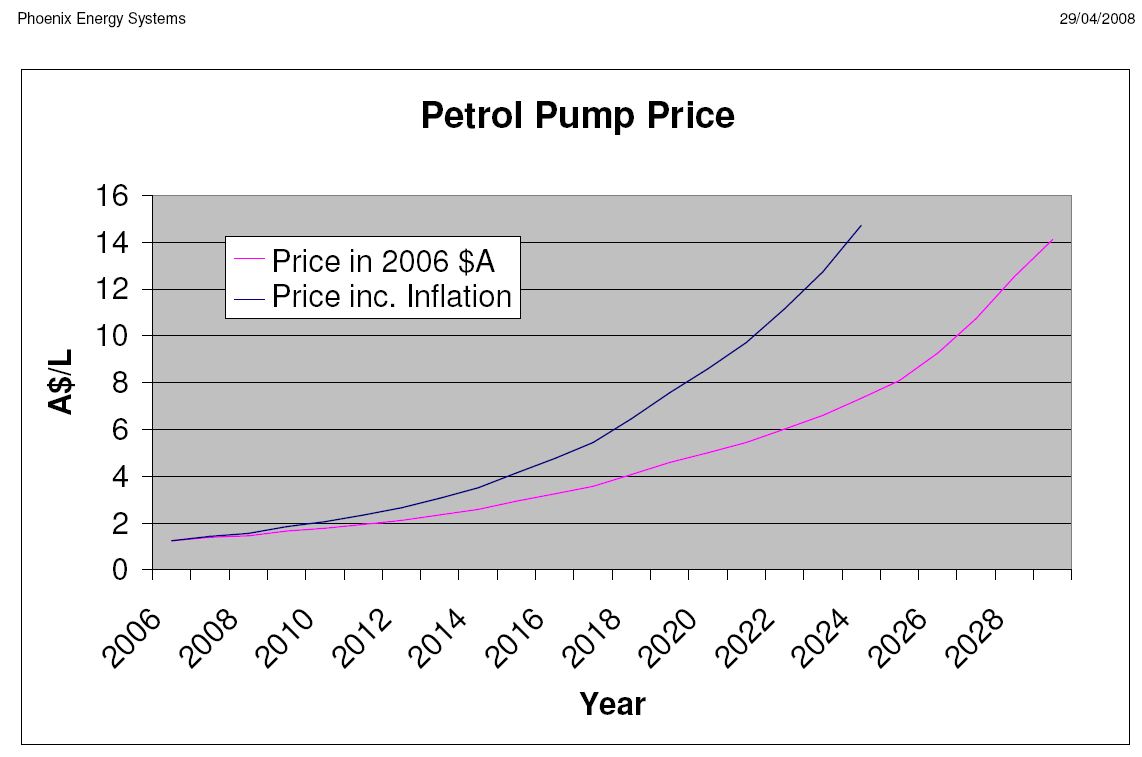

For Australian readers I have translated these numbers into a predicted pump price for petrol.

Click to Enlarge

Future Development

As can be seen from the above, the model generated suffers from a number of limitations (highlighted by *). For the most part these limitations spring from the extremely limited resources available to an individual. Yet despite this the results are considerably better than the IEA predictions.

In order to improve the accuracy of the model I intend to undertake the following revisions :

- Further division of the demand sectors with a separation of China/India from the non OECD group.

- Generation of separate sectors for essential services and perhaps agriculture in order to get a clearer idea of the likely effects government intervention may have on the demand.

- Incorporation of feedback on secondary demand destruction resulting from economic slowdown.

I hope the above curves form a useful discussion point for TOD members.

Contact

- anz at theoildrum dot com

License

This work is licensed under a Creative Commons Attribution-Share Alike 3.0 United States License.

Archives

- November 2010 (2)

- October 2010 (5)

- September 2010 (4)

- August 2010 (8)

- July 2010 (2)

- June 2010 (2)

- May 2010 (6)

- April 2010 (7)

- March 2010 (12)

- February 2010 (11)

- January 2010 (7)

- December 2009 (10)

- November 2009 (6)

- October 2009 (7)

- September 2009 (10)

- August 2009 (10)

- July 2009 (3)

- June 2009 (14)

- May 2009 (10)

- April 2009 (15)

- March 2009 (16)

- February 2009 (16)

- January 2009 (15)

- December 2008 (15)

- November 2008 (23)

- October 2008 (25)

- September 2008 (24)

- August 2008 (30)

- July 2008 (44)

- June 2008 (38)

- May 2008 (48)

- April 2008 (43)

- March 2008 (29)

- February 2008 (32)

- January 2008 (30)

- December 2007 (26)

- November 2007 (32)

- October 2007 (11)

Good post. I don't have any data precise data (no one does), but my years of experience, the research that I've done on Peak Oil (not allowed to reference my report here/stuff gets deleted/but you can find it), and common sense tell me that your forecasts are too conservative. Oil could hit $1000 in a few years after the peak, especially if some of the dire oil production decline rate projections turn out to be correct, see Jim Kingsdale's review of this: http://www.energyinvestmentstrategies.com/peak-oil/

and also the German Energy Watch study: http://www.energywatchgroup.org/Oil-report.32+M5d637b1e38d.0.html

ASPO is going for a slower production decline rate: http://www.aspo-ireland.org/index.cfm?page=viewNewsletterArticle&id=43

We will see soon enough, and even if you are on target, it's going to be a rough ride down. Hold on, cause alternatives are not coming to the rescue. Clifford J. Wirth

I would tend to agree. Even with oil at $120, large inefficient vehicles are still being sold and fleet efficiency is hardly budging.

I would expect a series of dramatic increases, followed by price plateaus as demand is destroyed to meet the new level of supply. We will get to 100 mpg plug-in hybrids by 2030, and if we do, we could support a oil price of $1000 per barrel because we will be using so much less per individual. Just imagine: $25 gasoline. Ouch!!

CLZ09:

This comment is, I feel, a little too pessimistic. What we need to do is look at the leading indicators and allow for lags. "Fleet efficiency", for example, is a function of all cars on the road. Given the way SUV sales were booming through the 90s & even until about 2005, we could expect fleet efficiency figures to be dropping as old, pre-SUV cars go to the wreckers. In these circumstances, having fleet efficiency being static is an indicator of how the graph is actually beginning to turn.

Second, sales of large inefficient vehicles are dropping. In Australia the local vehicle manufacturing industry is in hot water because it's based on making large 6 cylinder cars. Sales of 6 cylinder cars have been dropping markedly. Mistubishi has closed its factory. Ford & GM Holden have cut production and staffing. Ford has also announced plans to begin making four cylinder cars here - though it will probably take a couple of years for them to tool up.

Looking at the remaining buyers for 6 cylinder cars, they're mostly fleet buyers. If a car is sold to a households, it will be kept on the road for 20 years or more, probably going through 3 or 4 owners in that time. Fleet (note: this is a term used in the vehicle industry and is different from the usage of "fleet" above) vehicles, however, are usually run a lot harder and often are written off after about 3 years. At a certain price point for petrol, fleet buyers will shift away from the Falcons & Commodores en masse and the effect on average fuel consumption will be fairly rapid.

In Melbourne, the rising price of petrol has provoked a major switch towards public transport, to the extent that the sytem is now running at capacity. The newspapers are full of bitter complaints about over-crowded trains, so it is clear that even at present prices, there is considerable latent demand for a switch in travel modes. Invest in public transport and watch travellers fill the trains & trams as fast as you put them in service. As petrol prices increase, this will become an even greater pressure and will eventually overpower the road lobby.

Finally, the rising price of petrol is causing an increase in the geographic price gradient of real estate in major cities like Melbourne & Sydney. The first effect has been a reversal of the long-term trend for a decline in population density in the inner suburbs. This will accelerate. At a certain petrol price, people will decide that they are prepared to live in a shoe-box if that's what it takes to let them travel to where they need to be (e.g. work, study, essential services). While the outer suburbs will be full of McMansions that the owners can't give away, the city, the inner suburbs and certain other favoured locations will fill up with people rapidly:

* Luxury hotels which will go broke because of the collapse of the tourist trade will be converted to residential accommodation;

* People with large homes in inner suburbs but who are thrown out of their job through recession and/or Peak Oil undermining the economics of their industry will have rooms to rent. Before the inner suburbs became fashionable, there were many large houses which had been built 100 years ago as expensive homes for rich people, but had been converted during recessions to boarding houses. This phenomenon will return;

* High petrol prices will also bring about a resurgence in medium and high density development. Not only will demand skyrocket for good locations (as noted above), but fewer people will be able to afford to go up-market with renovations etc. The general level of maintenance of the housing stock will therefore decline and houses that come up for sale will therefore be a good deal more likely to be bought by developers.

There are some factors which will act as flies in the ointment, though. First, the Save Our Suburbs mob will do their level best to keep out the riff-raff by preventing medium-density development. Eventually their cries of NIMBY will be overwhelmed, but they'll be a drag on the inevitable adjustment process. Second, so much of the modern housing stock is based on open plan design, which assumes that energy is virtually free. Doors will come into fashion again when people find that they can only afford to heat one room in winter. This will be expensive, though, to retro-fit to all modern and renovated housing.

So, I'm not as big a doomer as many of the commentators here. People will adjust, though not without a lot of pain and even a substantial dose of bankruptcy. But adjust they will. If a couple have jobs that take them long distances in different commuting directions, one may decide to take a lower-paying job a lot closer to home because they'll come out ahead after transport costs are deducted. And so forth. People will have to adapt to a new lifestyle, but adapt they will.

You are probably right about the fact the significantly higher prices are possible.

The model I have generated is premised on there being a free and fair market in oil. There is no allowance for supply restrictions or market speculation simply because you cannot sensibly predict the effects of these actions. I prefer to think of these graphs as a floor price and these other unpredictable factors will drive the price higher than this level on occasions. The frequency of these occasions will grow over time.

Giddaye, Clifford (I see your name pop up a bit around the place).

I'm one of those Average Joe / Average IQ blokes that stumbled across the notion of PO sometime last year (curse that film, "A Crude Awakening"!). As a father of three, all I care about is my kids future, so have been taking an interest in sites like TOD to try and get some sort of handle of where the world is headed.

While I agree fuel prices could be seen as an indicator the PO notion is happening, I still find it difficult to accept for very simple reasons: The MS papers, radio, TV stations don't acknowledge it; very, very few of my friends, family or colleagues had ever heard of it (P. Coyle? Who's that? was one response); my mechanic doesn't believe it; and the owner of the local petrol station just rolls his eyes and says, "Nah, there's plenty of it left".

So I guess I'll just move on, business as usual and all that, wish all you TODsters the best and get back to sleeping properly at night. If nothing else, your stories have been great reading!

Regards, Matthew Blain (Melbourne, Aus)

Hi, Joe Average.

It's good to remember that there is always a lag between the discovery of new knowledge and when it becomes generally known.

As the price of oil continues its rise and if you should choose to come back to visit, you'll be welcome.

-Andre'

Matthew,

I recently went to a seminar where Richard Neville (hippy futurist)spoke about listening to the weak signals to really get the full picture. MSM does report on Peak Oil but they report the symptoms rather than the cause. You just need to learn how to read it. Drumbeat and the Bullroarer are fantastic summaries but theere is a motza of other stuff out there, which appears completely unrelated to oil, but if you follow the threads will lead back to oil.

At some point someone in a position of power is going to crack and say "What the hell is going on with oil. Don't keep feeding me the bullshit, I want to know what the deal is with $300 barrel oil. Why is it that high? it didn't just happen by itself. There must be a root cause" Then the MSM will be all over it and if if you have not prepared yourself by then, it will be too late. Options for the masses to make better living arrangements will rapidly close.

Journey Well.

Matthew Blain,

Well, First off I've got to say 3 things.

1. Your mechanic and petrol station are not a reliable source for economics or petroleum geology.

2. The average person doesn't give a shit or care, on average.

3. It has been all over the mainstream media if you've paid attention, but the MSM only puts entertaining like paris hilton on the front cover.

4. Seriously, if you wanted advice about your children would you listen to the MSM, your colleagues, the owner of the local petrol station owner or your mechanic, do some research and figure it out for yourself mate?

Let me ask you this?

Why would Bill Clinton, Warren Buffet, T Boone Pickens, Matthew Simmons, The CEO of Conoco-phillips, the Former VP of Saudi Aramco Sadad Al-Husenni, The VP of Lukoil Fedun, The President of Total, The CEO of Shell and 10 Congressmen, Several Mayors and cities and volumes of respected petroleum engineers, geophysicist and petroleum geologist all be concerned about peak oil while you shouldn't? Most people don't take the time to do the research but that's fine because their loss can be my gain. Good luck though

Swords,

Just finished watching "I Am Legend" with the wife (why'd it have to turn into a zombie movie?!) and thought I'd check in one last time before bed. It occured to me, might the bleakness of the first half of the movie be an exagerated expression of what life might be like after a few more decades of business as usual?

And that's my point. To me, an Average Joe with limited sources such as yourselves to converse with (further - and not to offend - it doesn't help that I don't know any of you from a bar of soap, much less all the respected names you mention) and though I completely understand Mother Nature only produced so much of the stuff, the concept of Peak Oil doesn't FEEL REAL to me. I'm not saying PO is nonsense - indeed, a tipping point makes perfect sense - it's just that at this point in time I find it difficult to accept: THAT LIFE AS WE KNOW IT MIGHT BE COMING TO AN END?!

It almost feels like an idea for a movie, a good yarn... Actually, as it stands, a conversation killer!

Swords, I AM concerned (about all sorts of things) and HAVE been trying to figure it out, which is why I've been visiting here these past months, as well as e-mailing local media figures (the sensible sounding ones that is, though not much return there. Even tried someone at ASPO - forget who - without answer). The trouble is I'm no rocket-scientist (clearly!), or a person of power or influence, or someone "in the know" and as far as the research goes, most of what you guys write about goes way over my head.

But even as I see oil hit $122 a barrel, while record car sales continue in this Land Down Under, I think what can I do about it anyway? Get smarter? How's that going to help? So FOR THE MOMENT, as I look out for the front-cover headline somewhere above the picture of Britney Spears, "World Running Out Of Affordable Oil", all I can hope is that you guys (and gals) are missing something.

But if you're right, at least I won't be surprised.

Cheers, Matt B

For the record, I take the education of my kids very seriously. The eldest (school captain last year) is at the pointy end of her class in an accelerated learning program - also plays a great game of tennis; and her little brother is hot on her heals. Such opportunities kids have these days. I hope they continue.

Matt,

I have three kids too and they all have great talents. But I don't sit around and passively hope anything for them. I take them out gardening. I teach them how to read whats happening around them to give them a bit of rat cunning. I teach them how to cook and how to use google to suck up as much knowledge as they can,just in case. I've adopted the no regrets appraoch to life. I don't teach my kids to be afraid of the future, I am teaching them how to be prepared for wahtever comes down at them.

You sound like you're just a little too attached to your comfy middle class lifestyle and not quite ready to accept the possibility that it all might go sideways any time soon.

As Phoenix says in his opening paragraph, all of us have gonne through a moment of shocked disbelief as we have absorbed Peak Oil and its potential ramifications. The truth is none of us really know what the future holds. By exploring the scenarios however you can learn a little bit each day and start to mitigate bit by bit.

I'm sure your kids are great tennis players, and I'm sure you're proud of them. BUt you need to ask yourself this question: If TSHTF have I done enough to give them the necessary skills to survive and prosper in a world where the oil ration is going to be severely curtailed?

And I don't buy your Joe Average excuse either. You seem like a pretty articulate guy to me. I suggest you go into Dymocks and buy The Long Emergency by James Howard Kunstler. Read it, absorb it. Take a week off work and recover, the come back and join us here on The Oil Drum for counselling and support.

OK Termoil, you've convinced me to keep the door open. But if it's OK, I'll still try and get some answers from local personalities - finance talking-heads, editors of motor magazines, presidents of car associations and the like (perhaps I'll even write to a few ministers, not that I'd hold much hope - the Australian Government can't even make a decision whether to ban plastic shopping bags or not!).

For the record, I read David Strahan's "The Last Oil Shock" late last year, which pretty well supported everything I saw in that film. Probably need to read it again along with your book suggestion. Also read Richard Dawkins', "The God Delusion" recently... Who's right and who's wrong about such things?

At the end of the day, it's still trusted faces and headlines that will convince me.

Thanks for replying, Matt B

PS. Don't Average Joes exist in "Middle Class"? That is, Average / Middle? I guess I am pretty handy with a trowel and hammer!

You read books. That alone puts you way past the "äverage" joe.

In my area, Northwest US, people fall into two categories when you talk to them about PO: those who have never heard of it and think you're a kook; and, those who have heard of it, don't believe it, and think you're a kook. Perhaps a lot more people would believe we have a PO problem if the powers that be in GOVERNMENT (not industry --> "gougers" -- and not Peak Oil Theorists --> kooks) would put their PR fears aside and make an unequivocal statement that PO is here and we have to get serious about the problem. Of course, fat chance of that happening...

In the meantime, they are merrily buying SUVs and giant pickups -- and getting great deals!

Thank you for sharing your model. I like the pragmatic engineering feel of it. FWIW in my personal experience as an engineer, your approach often yields a very close model to actual for at least short time frames of 2-3 years. In years out beyond that, more possible error, but empirically it sure looks like some parts of the base model are dead on. The whole competition for finite resources is core to your model and is what I expect to occur. I wouldn't give economists a second of thought or any respect. As some later commentator put it, they'll come around in a few years but the conservative nature of most highly paid economists is detrimental to making progressive insights using the frightening data that is accumulating now.

I did a conversion to USD per gallon and you can simply multiply A$/L by 4 to get USD/gal. I think the gasoline prices in USD/gal sound reasonable too. It keeps sneaking up over the next few years but by 2016 the hurt will be felt by most in USA (they'll feel it sooner than that but realization that TSHTF is really spraying brown all-day, every-day will likely take much longer, IMHO :-/ )

I agree with other posters, if you would be willing to share the actual Excel spreadsheet, this would radically help more discussion and evolution of the model. I'm not sure if you are seeking recognition or using the model for personal gain & planning. It really is a good chassis and could foster more development and thinking. So please dare to share. (Not to mention clog up TOD for a while with hot discussion :-)) It would be fun to watch though!

Interesting work.

Is it possible to share the actual figures on the assumptions you have made, especially the rate of renewables substitution?

The substitution rate is not as simple as a fixed dependancy on oil price. Unfortunately it also has a significant time lag. I have tried to model this time lag.

In terms of real numbers I have a total (renewables plus substitutes) of 6.3 Mbpd by 2020.

Thanks for the reply.

I understand that you are in a somewhat delicate position being employed within the industry, but I wonder if it would be possible to post the spreadsheet showing all figures and assumptions?

Anonymity would still cast it's kindly cloak!

Anyway, many thanks for what you have so far shared and the valuable insights it gives.

This is impressive work, using sterling logic. It is limited only by the lack of accurate information.

I was wondering if you might explain what role a bell curve plays in your calculation. I did not realize that statistical analysis was required for a prediction of this kind.

You point out that, in a hard-scarcity situation, a commodity price is set by the threshold at which successively stronger low bidders drop out of the market. That simple point should be disseminated. I hope it receives some attention in the world press.

Sadly, in the U.S. no major media company is likely to publish anything so terrifyingly clear and logical on the subject of commodity allocation. Any such revelation might rattle the cage of denial in which we USA-ans are expected to remain confined indefinitely. The real sin against "patriotism" here is to reveal some fact that threatens to discourage the populace, even momentarily. Like any confidence game, the "demand-driven economy" is mortally afraid of reality.

Well, I'm a reporter with Wired, and I'm (at least) thinking about it... (Not to derail the main discussion but here's the problem with something like this making it into the MSM: A) It's hard to know how to get into a story of this magnitude as B) editors are not exactly prone to running stories about models C) from anonymous sources, even ones that clearly have done some great thinking and analysis.

If Phoenix were willing to go on the record with his energy background fully presented and send his model to some economists or other specialists, etc. Then we could really get a story going. Just saying.

I am an analyst with one of the Big Four. Phoenix's model would not survive contact with our economic analysts because:

1. It is still too immature and relies heavily on guys in the industry providing a "best guess".

2. It flies in the face of everything we have assumed thus far.

The fact that phoenix's model has made better predictions than anything that we have come up with is really immaterial at this time. I am not trying to denigrate my colleagues - they are intelligent, hard working and generally open to new ideas. Eighteen months or two years from now they will be willing to talk about this idea. But not today.

I will contact phoenix and ask him to reply to you, but all of us have jobs. We need to buy farmland out in the country, install watertanks etc. A "career limiting move" might not be what phoenix has in mind. Anyhow, I will contact him and let him speak for himself.

The ABC news tonight had two separate price predictions Goldmans: $200 and CitiBank: $40.

I think one of them needs you Phoenix - great post.

...and the last time I heard oil prices mentioned on CNBC they called it a bubble...at what price point does that end, $200 or $40? I think they are going to stall until one or the other is reached...too much rides on their opinion, like advertisment revenue associated with a rising stock market.

Once they stop calling it a bubble, it will burst..

Think contrarian.

Sixteen years ago, while attending a composites conference, I sat next to the Director of Advanced Engineering for GM. I told him that if he wanted to see a paradigm shift in his industry, he needed to hire some farmers, because farmers solve engineering problems all the time but most haven't been to engineering school, so they don't know the "correct" way to solve a problem. They go ahead and solve the problem anyway, often in very creative fashion, because their minds are unconstrained by conventional ways of thinking.

I've noticed that economists tend to have a very narrow education, being grossly lacking in botany, biology, anthropology, geology and environmental science in general. I wouldn't be too concerned about the evaluation of industry economists of Phoenix's oil price model. It's obvious that the entire industry is caught in a rut, a particularly virulent example of group think, and will have to be rescued from the outside.

Fred Schumacher

retired farmer

member, Mankato (Minnesota) Peak Oil Task Force

Alexis,

Here's the rub, or the caution, having economists review the theory. There are some that would be willing to look beyond orthodoxy, but they will surely be countered by the traditional "balanced opinion."

I feel somewhat qualified to comment on both areas as I am an engineer and I minored in economics. Phoenix's perspective is dead on about the traditional economic models that seem to be based on infinite supply. I had the same gut feeling this wouldn't measure up in the long run.

Wired hasn't been shy about publishing controversial subjects, but I guess this hits too close to home for many. Frankly, I don't like looking at those price projections either. I think there has to be some major disruption to cause a redefining of the model (i.e. war on a major multi-national scale).

A result of my undergrad thesis was the very beginning of dynamic modeling technology. The postulate based on experimentation and good old number crunching was that highly complex systems cannot be defined by a static model over time. The boundary parameters can remain static, but their functional relationship can change, thus causing a reshaping of the functions such as feedback, motive force, output level, etc.

In retrospect, it could be the physical proof of the axiom linear thinking is dangerous.

I would hope influential academics and professionals would take your model into serious consideration. Too bad being just plain right versus far off straight line projections ought to be enough. It is sad, really sad that prurient interest is more important than fulfilling one's duty to the public good which is a cornerstone of professional obligation.

I can't wait till I get my model together what I found is that complex systems post peak are almost impossible to model but they fall into two major groups collapse and a exponential decline. The latter arises from the central limit theorem. The former from the massive amount of coupling that takes place when a complex system becomes resource constrained especially if the resource is not renewable or has a renewable rate greater than the consumption rate. Despite the literature on collapse most of the approaches fall into a predator prey model that only deals with one type of feedback loop. I've not been happy with the literature on the collapse of complex systems. I've come up with Nate Hagens with a concept of coupled logistic functions that get steeper over time as extraction rates increase. The final collapse is the result of effectively eating the last supply of the resource with the final logistic. The nice aspect is it seems to keep both consumption rate and the population of consumers high right to the bitter end.

More generally it seems that the system becomes a group of coupled harmonic oscillators with increasingly steep wells or increasing frequencies. Think of turning a thousand amped microphones sitting together on cranking the amplifiers and the feedback loop.

A experiment I'm keen to perform :)

The opposite case of a exponential decay is a group of oscillators that become uncoupled and generally widen effectively disappearing over time although they are uncoupled so some can sharpen and disappear. But in my opinion this requires a really slow change like a decaying climate. If you think about it post peak aggressive moves will be made to decouple the global economy as fast as possible so the decoupling case is easy to understand and it matches the central limit theorem thus collapse must be the coupling case by default the central limit theorem actually eliminates all other cases except the one where it does not hold i.e coupling.

In any case I'm giving away my punch line to prove collapse you only need to prove coupling and thence the central limit theorem does not apply.

Could somebody interpret memmel’s manifestos for me? It’s as if he transmits FM and I receive Betamax. I like his ideas, but I often feel like I’m bobbing for an apple when I read his posts.

No disrespect intended to memmel, it’s just … I’m not getting it.

Fractional Flow left me feeling the same way. Other drummers helped me get the goosebumps. So if you “get” memmel, could you restate his ideas in your own words? Thanks.

Cold Camel

Heh, you said exactly what I was thinking :)

My take on memmel's post was that "coupling" is another word for business-as-usual globalisation, with economies based still on provision of credit, on just-in-time deliveries over large distances instead of stored inventories, on "growth".

By clinging tighter and tighter to those BAU methods, society will in affect be pushing down on the accelerator and careering headlong over the PO cliff ... at which point the finance system is irretrievably broken, JIT has failed, and the debt for our pursuit of infinite growth has been called in -> sudden and precipitous collapse.

"Decoupling" is a move away from globalisation & back to localised economies. Personally I doubt there's many places in the western world that would be capable of this - we've all become hooked like junkies on international trade to supply things we can't grow/build/pump ourselves. That aside, if an economy is decoupled its less prone to a domino-effect crash, but suffers from its own limits.

That's my take, which may or may not be more readable than memmel's post, and may or may not interpret his words correctly :)

Well, a complex system could fail in two ways. One of them is failing completely, when a small failure of one component leads a biger failure of another and so on. This way, everything goes down quite fast. The other way is from partial failures, where failure of one component leads to a smaller failure of the others and so on. This way, you have some troubles, but will end with a set of simpler systems at the end.

Also, he describes a precise mathematical model for both kinds of failure and proposes that the model may help we discovering what kind of failure to expect.

For non specialists some of the terms need defining for this to make much sense.

I look forward to when you have the time to lay your thoughts out in more detail.

The one which springs out as needing definition are 'central limit theorum'

The distinctions between the two models and how they relate to the central limit theorum are also unclear, as is the relation between this and other posts indicating that collapse would be fairly limited.

I think I have the general drift but can't be sure.

Just saw this and thought I may be able to help...

The central limit theorem (CLT) is a result in statistics that describes the result of averaging independent random variables. Roughly stated, one version of the theorem says that the average of N independent outcomes of a random variable with finite variance (a technical assumption), will approach a normal (gaussian) distribution with variance that scales as 1/N. Think of flipping a coin a large number of times, counting 1 for heads and -1 for tails, and averaging the result. The central limit theorem says that the average will behave like a bell-shaped distribution around zero, where the variance will decrease as you increase the number of times you flipped the coin (the chance of the average being far from zero will get smaller as you increase the number of times you flipped the coin).

This result only holds if the trials are independent ... imagine flipping 100 coins that were somehow glued together so that they all landed heads or tails together. Then the CLT would not apply, and the average value of the experiment would not typically be close to 0.

I think this is what memmel was referring to with coupling ... if global systems are decoupled then the outcome of collapse in one location of the earth will be independent of the outcome of collapse in a distant location, so one could use the CLT to get an "average" collapse condition that would make sense (i.e. many areas would be close to the average condition with high probability). But if the global system is "strongly coupled" through trade or financial networks then the outcome of collapse in different locations will not be independent, so it is more difficult to describe an "average case" outcome. Or, as the CLT wouldn't apply, there may be no reason to expect that the situation in any one place would be close to the "average case". We would all sink or swim together.

If I've misinterpreted what memmel was saying, I apologize.

Thanks for the reply.

In that case then you would have a whole range of likely outcomes depending on the degree of coupling - results are strongly normalised for a sequence of 100 coin throws, but less so for 10.

There is also the thought that although the collapse in a strongly linked system might be universal, the outcome might not be, as within particular societies the degree of linkage will vary.

For instance, some are nearer to subsistence agriculture than others, so the result of a collapse might be a return to the village, whereas other societies are much more heavily dependent.

IOW a universal collapse might itself imply the creation of a less strongly linked system, so at later stages a whole variety of results will obtain.

The effects on someone living in New York City will be different to those in small-town Middle America, although the impetus might be common.

Nah, sorry didn't help but thanks for trying!

Thats exactly what I'm saying I should add that most people think that WestTexas's ELP ( Economize,Localize Produce) concept makes a lot of sense from my approach it seems to have very strong mathematical support. Somehow it seems he nailed it.

But the reason I was more generic is this does not only apply to economies it also applies to oil extraction. How oil is extracted once a region has past peak is strongly coupled in many ways. The first coupling is simply attempts to maintain and increase production at the global level regional production effects price etc. If you buy into a coupled global economy then you realize that the oil industry is the most highly coupled global industry on the planet.

Think about that for a bit.

Memmel

Your model sounds similar to the work done by Didier Sornette to use complexity theory to predict earthquakes, which he has then used to understand stock market crashes and housing crashes. I didn't investigate all the maths, but the basic signal was an overall up trend with an oscilation about the trend of increasing frequency. My guess is that your coupled logistic functions might come up with the same type of signal, but I may be reading too much into this.

Still the article is intersting anyway if you want a different view to how stock markets work from the standard economic textbooks.

Long article

Shorter article with charts

Jeremy

Hi Jeremy,

Thanks. My short Q: has the oscillation held as predicted? WRT oil, I don't know but my impression is, it hasn't, really. Just up and up.

I don't have the link but for whale oil found this but its not the original.

http://www.energybulletin.net/3338.html

The price range was 200-1500 a barrel. Pretty much in the range ware are talking about for initial post peak prices.

I'd say we are in the very early stages of post peak oil pricing. Simple analysis of disposable income and the lack of change in demand avert a 500% increase in price means that we have not even come close to prices levels that cause

demand destruction. If I had to guess we won't see the oscillations until oil is over 300 a barrel at least.

A better metric is when the world is clearly down by at least 2mbd and its obvious that we are probably post peak.

This is the point that real post peak pricing fluctuations become possible. Right now I'd say the market is slowly realizing that oil might possibly be a precious non-renewable resource.

Your links are fakes :)

I found this.

http://www.jsmf.org/grants/cs/essays/2000/sornette.htm

I did not find the actual theory paper but will dig.

Thanks.

alexismadrigal,

I was thinking about MSM attention to the idea that limited supply necessitates price increases until the necessary number of bidders drop out. (More precisely, the sum of bidders dropping out multiplied by the quantities not purchased by each of the dropouts, must equal the shortfall.)

This is a good approximation as long as the wealthy purchasers do not change their buying habits much.

Since the US, as the largest consumer, is not yet dropping its usage significantly, I suspect the price will continue to rise until there is some demand destruction here in the US. If that is true, we will see the price continue to rise in the near future.

Your forecasting the price of oil to be about 150$ by the end of this year, that sounds about right to me. Although you might want to take into account falling net exports which will decline faster than production. The total production doesn't matter much compared to whats available to buy on the oil market. I'd like to see your results once you include that. If you need some resources on that you should check out the Export Land Model or ELM. Good Work

http://www.theoildrum.com/tag/export_land_model - post on ELM

These are a very scary set of predictions but to evaluate them, I guess we need to see your assumptions on demand destruction and alternative growth rates.

From a technical perspective there are a variety of technologies that provide transportation with a far smaller liquid fuel requirement and various alternative fuels that could replace crude oil. The question for both is what is the take up rate for them?

Can you show us some graphs with these assumptions too?

I can imagine 20 KB/day CTL in Australia by 2010, rising to 100-200 KB/day by 2015 and many hundred KB/day by 2020.

Those prices would make such ventures astoundingly profitable.

The problem with CTL and Tar Sands and other such alternative fossil fuel and renewable ventures is while if the fixed cost of operating such a venture remained the same then yes they would remain pretty darn profitable. However, such higher oil prices is going to feedback into the system and make these ventures not a profitable as one might think. The cost of energy is going to drive up the cost of all the materials and stuff required due to inflation driven by energy. The profits are not going to be as insane as anyone thinks because they think in 2008 based cost and 2020 based profit...

Australia used 877000 barrels of oil a day in 2007. That is 140m litres. 200k barrels is 1/7th of 1%. Probably will not matter one way or the other.

That's 200,000 Barrels per day of CTL, so that's around 22% of 877,000 barrels per day.

OK, I'm convinced -where do I put my money... :o)

[Or put another way: which CTL companies look set to make a killing, I know of only one: Sasol of South Africa]

Nick.

I covered CTL (particularly in Australia) recently here:

http://anz.theoildrum.com/node/3817

This is good work, but not very useful since you don't account for falling exports. Exports will decline faster than production. By 2030, global oil exports will be approximately zero (refer to WestTexas's ELM).

Can you redo your calculation considering exports instead of production?

Also, I don't think any model will be valid after everyone comes to know about peak oil. In about 5 years I expect governments to intervene and impose rationing, etc. which will change the dynamics and invalidate the simple demand/supply model.

Either way, please keep up the good work.

Phoenix's numbers do not go past 2030 because he agrees with you. He refers to it in different terms, but a full explanation of everything that goes through your head as you write would lead to a 20,000 word article (a problem that I struggle with regularly).

Taking into account the way consumption is prioritised due to limited supply (ie country of origin, then military, then government, then agriculture, then industry... etc) is possible with this model, but sadly phoenix has a day job... so it may take a while.

I have read some of the work on the ELM and agree with much of the conclusions. The concept of ELM is that export nations will essentially separate themselves from the world market for oil. My model is based on the idea that the price you pay for a barrel will be the same in Australia or the US or Saudi.

You could create a model that takes into account only the external trade portion of the market. But to do this you would need to look at each individual nation in the same way that I have looked at the OECD and non OECD. It could be done but it would take a lot of effort.

Thanks for the response. I don't think you have to look at each individual nation. You can look at two hypothetical nations, viz., importland and exportland. Westtexas's ELM model tells you the rate at which net exports will decline every year. You can then put that information in your spreadsheet and calculate the price importland will have to pay to win the bidding war for declining exports.

My premise is that the price of oil is being set at the margin as importers bid against each other for declining oil exports. To add fuel to the fire, the price of refined products is subsidized in many exporting countries, but once production starts declining in an exporting country, my simple mathematical model (ELM) and several recent case histories indicate that the the net export decline will be rapid no matter what. For the ELM, I assumed a 2.5%/year rate of increase in consumption (resulting in net exports going to zero in 9 years). Even with no increase in consumption, net exports would go to zero in 14 years.

In the importing countries, let's divide all consumers into five groups, and rank them by income. At the top of the top quintile, we have consumers like Bill Gate. At the bottom of the bottom quintile, we have a poor Third World consumer. Imagine the price necessary to force Bill Gates to conserve energy, versus the price necessary to force the Third World consumer to conserve. As forced energy conservation moves up the food chain, the upper quintiles have vastly greater buying power, which requires an accelerating rate of increase in oil prices, in order to balance supply & demand. When we combine this factor with an accelerating net export decline rate, we get, IMO, a geometric progression in oil prices: $50, $100, $200, $400. . .

The only real question is the time period between the doublings.

Each of the quintiles by wealth would also have an energy use profile. The rich quintiles would be the bigger users of oil and have more ability to tolerate the higher price without it becoming a budgetary factor for them. If you were to quantify the use of exported oil this way, you could actually try to model the bidding war for oil as it moves up the buying power range.

You'd probably see that it's pretty hard to get much demand destruction in an oil price climb. This was abundantly demonstrated during the 1970s. Here, against a global economic backdrop wracked by severe recessions, no China explosion, no India, you had a demand and price surge in oil just from the motoring increase by the land barges in the U.S. and pre-BRIC consumers. It was not "the embargo". There was no embargo that lasted the whole decade. On the contrary, the Arab swing producers strained production beyond safe limits to deal with this demand surge. Yet the price of oil climbed 900% during this 10 years. By the conventional wisdom discussing demand destruction today, this price climb should have crushed the consumption of oil. What did global consumption actually do? It suffered no destruction at all and, in fact, climbed at more than a 3% per year rate before the death of the land barge and a recession caught up with it in the early 80s.

This ELM/bidding war effect in todays BRIC world, not to mention the fast approaching net energy cliff thing, could produce more of a climb in oil price than we think is reasonable.

As I was reading this, the thought struck me that, perhaps, there is an inverse correlation between global per capita boe availability and the price of oil, that is, the price of oil will go up as the amount available per person goes down. This is sort of a take-off of Richard Duncan's Olduvai Theory.

Todd

Well my approach is not to different but I start at the end game and work backwards.

I assume a assured supply of 40mbd at some point in the not to distant future.

I assume that 10-20 dollars a gallon in 2006 dollars is a reasonably price for just about any renewable replacement for oil.

Add in a 50-100% shortage premium and you get a maximum possible price of 40 dollars a gallon.

In any case 20 dollars a gallon for gasoline equates to a price of about 600 or so a barrel.

At the end level diesel for farming or other critical needs will distort the pricing picture quite a bit but much over 20 dollars a gallon seems to be the price at which renewable approaches are very competitive and the amounts used are low enough that renewables can replace.

So you work backwards from that. The next assumption is effectively no real demand destruction till prices climb over 10 dollars a gallon. You will have conservation but at best this will only cover growth in economies in India and China.

So I think your right about the bidding war but wrong on the price points at which demand will really begin to fade.

And next the point at which viable substitution seems to happen is at least above 10 dollars a gallon given the fossil fuel inputs that would be needed for agriculture probably closer to 20.

Between where we are and 10 dollars a gallon for gasoline your not looking at any real reason for price increase to stop.

In the US it means moving closer to work and ditching the SUV in Europe and Australia similar belt tightening but less of a impact. In short the most flagrant waste can easily be excised up to about 10 dollars a gallon. Considering cars getting 40mpg. Economies will slow and effectively be in a depression but other than that I just don't see points at which the price can back off. Any drop in price would quickly spur suppressed demand.

So I think its not hard to find reasonable limits to fuel costs. Although scary to your average McMansion/SUV driver they are not high enough to cause the end of civilization.

So what is the impact ? Assume that gasoline triples in price in the US from 4 to 12 dollars assume that fuel costs are 10% of the economy you would need a 5% economic contraction to in effect absorb high fuel costs. So this is spread over 2-3 years and your looking at say a 2% retraction or so each year. So a negative GDP of 2% a year which is a combination of both money absorbed in higher prices and reduced business activity is more than enough to handle even alarmist price increases.

http://calculatedrisk.blogspot.com/2006/07/energy-consumption-as-percent...

So going from the end and looking backwards I don't see any real issues with prices getting well over the 400 a barrel range over the next few years and 800 by say 2012-2014 is not unreasonable and can be handled. At that point real substitution is very attractive and usage should be down enough to make it feasible.

Given that no real barrier exists to prices rising north of 400 a barrel I think that if you factor in Export Land etc your optimistic by twice the number of years.

Finally prices have risen 500% in the last five years without substantial decreases in production. I think assuming a 500% increase within 3 years is not unreasonable at all given real declines and export land. That puts you at 500 a barrel by 2011. Assuming 500% in five years which matches the past gives 500 dollars a barrel by 2013 and you have it at 2020 in your inflation adjusted dollars. Basically your non-inflation adjusted numbers are probably correct real numbers since oil prices are fairly immune to inflation over even a 6 month scale. Considering the nature of oil I don't consider it possible to really change the price over even fairly short lengths of time with monetary inflation.

Fine analysis, Memmel.

I have never quite understood how the doomers get to what they feel are the inevitable consequences of peak oil, although of course many are totally disenchanted with our society and have little interest in it's continuance.

If we make enough dumb decisions we could certainly tip over into breakdown, but it seems to be by no means inevitable.

On a different note, do the figures you have just given include allowance for the increase in other fuel costs, and the knock on effects on everything from food costs to a build for renewables and nuclear?

It seems the approach i have used is very similar to your own. I have just been a lot more detailed in the calculation of the "shortage premium" by breaking it down into economic and industry groups.

I am not sure I agree with your statement "oil prices are immune to inflation over even a 6 month scale." It depends on what your definition of inflation is. A large portion of the huge oil price increase over the last 6 months can be attributed to the weakness in the USD. Maybe I have misinterpreted your last paragraph.

To be clear attempts at monetary inflation will backfire with oil leading to price increases. By this I'm talking about devaluing the currency. The price of oil will drive higher to overcome any attempts to inflate away the real cost of oil.

What a lot of people think of as inflation which is increasing wages and prices is not happening. For example the latest attempt at monetary inflation by lowering interest rates has lead not only to a spike in oil prices but a fall in real wages as wages remain stagnant or decreasing and more important consumer credit is undergoing a massive deflation. Its wrong to look at price inflation for goods and services vs oil since high oil prices spur that inflation. The best metric is percentage purchasing power devoted to oil. Using that metric its obvious the real cost of oil has risen dramatically over the last year. A simpler measure is percentage income. But this is not correctly adjusted for price inflation of other goods that require oil.

For a lot of Americans that have lost their HELOC and maxed out their credit cards gasoline and food now take all of their disposable income. On this basis many have seen percentage expenditures on gasoline increase by 100% or more. Real purchasing power for many has dropped several hundred percent via loss of Heloc's move to lower paying jobs and increased costs in general wages have been stagnant to declining etc.

This is the number that matters on a bigger scale its the number of people hitting this wall. This has also increased substantially. The only thing they can do now that they have run out of credit is move to cheaper housing and try to purchase cheaper cars. This group in effect are the first lemmings to fall of the cliff with more to follow.

Its not the end of the world for them but its the end of their existence as a member of the consumer class they are reduced to whats considered subsistence existence in the western world. They pay rent gas food and electricity and cable tv with effectively nothing left and use payday loans and pawn shops for credit. But this is a critical point these people are at the edge and cannot afford any increase in cost. At that point generally what happens when the attempt to ride the bus or take other transport they lose their job. Most employers won't even hire you in the US if you don't have a car. Eventually the an emergency tips these people over the edge. In a growing economy the can struggle forward by working overtime taking a second job etc but in a shrinking economy its difficult to do this. This is your inelastic demand that your interested in that only stops via effectively catastrophic demand destruction. And as I said its measured as a percentage of income.

Now here is the problem the oil usage by even these people does not change all that much vs wealthier classes. The minimum amount is surprisingly high. One of the reasons is most families are dual income so moving close to work is not possible since their jobs are not close together. One spouse may move close to work and not drive but the other is often left driving quite a bit. This potentially eliminates a car payment but with many jobs spread out into the suburbs one long commute is common. And of course most of these people work in the service sector which sells goods and services to a rapidly shrinking middle class with disposable income. So you can see that at least in the US the real cost of gasoline has seen a dramatic rise using my metric which I feel better reflects both the economic hardship of high prices and inelastic demand followed by real demand destruction as it becomes uneconomic to drive to a low paying job. Taking that step is a tough one. But this is where people finally seriously cut their oil usage they either manage to work and use public transportation if they are lucky or the quit working. Since demand cannot exceed supply oil will increase in price as needed to force as many people as needed over this edge. This price is much higher than your approach suggests.

If you play with various scenarios given income level of 15k-30k numbers of people in these income brackets and living expenses its pretty obvious that nothing keeps gasoline from hitting 10 dollars a gallon given that real declines in production are forthcoming Indian and Chinese economies will take a while to reach negative growth and export land.

Some get pushed over right now a bit more at 5 dollars a gallon but you have to take it all the way to 10 to force a significant percentage to the edge so they fall over.

Just a quick example.

Wage 12 dollar a hour 40 hours a week = 1920 a month lets be optimistic and throw in some overtime so average take home is 2000 a month. Or 23k a year not a bad wage.

You can get some real numbers here.

http://community.stretcher.com/forums/t/4326.aspx

Housing 500 Utilities 200 Food 300 Car payment insurance 200 Phone cable 60 Credit card 100 ------------------------- 1360200-1360 = 640

30 miles a day 30mpg = 1 gallon a day = 4 dollars a gallon = 120 for gas

120/640 = 18% of disposable

At 5 dollars a gallon

150/640 = 23%

Now this is a direct 5% loss in disposable assume we see a general price increase of 5% as fuel cost passed on.

Say it hits food and utilites they where 500 they got to 525 So the real cost is

175 not 150 so the real precentage is

175/650 = 26%

Now it gets worse store hours are cut back so no overtime buddy sorry and in fact I'm going to cut your hours some.

Lets say this takes us down to 1800 take home from 2000 so you lose 200 a month.

650 - 200 = 450

175/450 = 38%

So gasoline cost when from 18% of disposable incoem to 38% or basically a 50% increase and this dropped your money available for consumer spending by 50% !

Now what does the price of gasoline have to go to to force this person to quit driving ?

A first estimate

450/30.0 == 15 dollars a gallon. But do a bit more of food price inflation and say lower the work week to 30 hours gives

1440 a month assume that he manages to take all this home with a few 40 hour weeks assume just a 0 dollar increase in food costs he is eating cheaper.

1440 - 1385 = 55 dollars at 30 gallons a month he needs gasoline prices to be 1.83 a gallon.

He is toast with this scenario so let throw him in the unemployed pile and start over.

So lets cut his clone some slack but its obvious that however you play out the scenario this worker is right on the edge as gasoline crosses say 7 dollars a gallon not 15. You can see where I come up with 10 dollars a gallon based on a 30k starting hourly wage.

But since supply equals demand

http://en.wikipedia.org/wiki/Household_income_in_the_United_States

68% of Americans earn less than 25k Gasoline prices will rise quickly to the 7-10 dollar a gallon range to take these consumers out to balance supply and demand. You see that percentage of disposable income is the critical metric.

Demand destruction may happen elsewhere at lower prices but the poorer regions tend to be less dependent on gasoline and can do substitution given the amount of oil the US uses its the American consumer that has to be taken down before the rate of increase in oil prices will begin to moderate. To take out the next level which has probably fallen given the high prices requires heading albeit at a lower rate into the 10-20 range. Only at this point has the pool of consumers been reduced to the remaining upper middle class and they have reduced their demand. But the next big group is the 50k range which is 45% of the population so to take this one down requires the doubling of prices again into the 20 dollar range.

So however your figuring the price of gasoline and the oil price required in my opinion my approach pretty much tells you the price points that will wipe out enough demand to match supply so its pretty obvious that prices will rise until they accomplish the task. On the positive side if any its also clear that you don't have a lot of reason for prices to rise much over 20 dollars a gallon since the percentage of the population that can afford that is small esp in a devastated economy.

A lot fewer people will be in these upper income brackets and your consumption has dropped low enough that alternative fuels can finally supply a significant percentage. And obviously the government would have been forced to provide better public transport car pooling and a real movement back to the cities would have happened at this point.

US demand would have been effectively cut in half from 25mbpd to 12mbpd probably lower. 30% -50% of the population is living in poverty so you effectively have 3rd world demographics in first world countries in fact the US demographics seem like they will closely match Brazil's current demographics. God only knows what happened in the 3rd world at this point basically subsistence living for many given the low dependence on oil however they may actually fare better than expected.

But believe it or not it pretty much stops here. Further development will focus on supporting a oil free society so overall things get slightly better. Its not the end of the world just the end of the first world. Now throw in a touch of global warming and things get quite a bit more miserable but still potentially generally livable if you can stay out of squalor.

You forgot to mention that the 30% to 50% of the US population that are to be living in squalor will be highly pissed and armed. And the idea that our nuclear-tipped military industrial complex will not die quietly.

memmel, I think you are pointing up the short term change that I saw when I began modelling this. At some point in the not too distant future the US poor will begin to find it impossible to afford their vehicles. Maybe they will substitute, maybe they will crash. It all depends on their baked-in level of discretionary spend. After the past few decades, I think that is less than your maths assumes - people have signed up contracts that lock them into break even spend, or close to it. Their demand will fall away (already is) and US consumption will actually fall for a number of years.

The point is, if you are modelling future prices you need to include such effects within the model. I expect that the fall in demand will result in deep recession, economic problems in China and India as a result, and thus a larger drop in global oil demand. All that will produce a plateau in prices as oil exporting countries recognise the coming decline and take the opportunity to cut back on production to keep prices stable and conserve capacity.

In short, to model this well you HAVE to include the various feedback loops and delays. They drive the shape of the curve and determine the change of attractors (from a CAS standpoint). Simple differential maths can't hack it, we're entering a period where things will flip instead. A good model doesn't spit out smooth curves in that environment.

Your analysis seems great for the US, and perhaps Australia.

It would not seem to apply to Europe, as not having a car does not usually stop you having a job.

This does not apply to a lot of people in rural areas, or some who use their car in the course of their work, but for most of us we would just put up with the inconvenience of catching a bus.

Food and residential fuel costs will hit poorer people hard, and the consequent recession throw lots out of work, but he effect would not seem great enough to create third world conditions in most of Europe, or in Japan.

Not having a car does not stop you having a job in much of Australia.

I've only had one job in the last 10 years that I drove to work for (and that meant I had a 30 minute drive instead of a 1 hour train trip, so it wasn't like I couldn't have used public transport if I couldn't afford the car trip). I don't particularly like commuting by car so I ditched that job when my contract renewal came up (the company had moved location) and went back to a job where I had a 10 minute train ride instead.

High fuel prices will adjust the parameters people use when deciding where to work and where to live - there is a lot of slack and waste in the system that can be reomved to cope with declining oil availability / rising prices....

Memmel - I'm out travelling - left a note for you on Luis' coal crunch thread.

Interesting stuff. What is your chart showing? The numbers add up to about 150. Further breakdown of the $25K+ (whats that?) group would be required. Does minimum wage distort the picture here - meaning that a large chunk of the US population fall into poverty simultaneously?

And what $ / barrel does $10 / gallon translate to?

Memmel misread the graph. It describes the percentage of US earners over each amount. So 68% below 25k is actually 68% over $25k.

I actually agree with the analysis - it will get nasty for low income folk, but the numbers affected are small to begin with, less than half the numbers memmel quoted.

I read the caption again and I think your right its not 68% but about 30%.

And that just means the price has to push higher to match supply and demand. The number effected is constant.

All that changes is the price points.

Found another similar grouping.

http://www.econlib.org/library/Enc/DistributionofIncome.html

So about 30% looks right.

Dyslexia strikes again.

I believe poverty is set at 15k.

But understand what your saying is that prices have to climb higher to cause demand destruction.

You have a larger population more resistant to price increases. Also although I did not work it out disposable income does not increase all that rapidly as you go higher in income in general housing/car/food expenses simply increase.

Credit becomes more available and more income becomes devoted to paying credit card bills.

I work it out for hypothetical cases that use realistic numbers. So basically doubling the income results in it getting fairly equally distributed on a percentage basis.

So

20k == 400 disposable per month

40k == 800 disposable

80k == 1600 disposable (this is probably now high if you include taxes and affluence)

Notice that the 40k group is twice as resistant to high prices. You cannot dismiss the housing bubble and credit bubble since this has eaten heavily into disposable income for the 40k and higher crowd.

As has been stated many times here at TOD due to higher taxes we here in Europe are already paying double or triple the US rate (UK: $10+ / Gallon). I see no real demand destruction yet.

It's possible that as prices rise some of the taxation will be cut out of the final pump price in order to relieve the burdon as the 'base price' (non-tax) signal will be doing its work of cutting demand. For example we have a 70%+ 'taxation cushion' here in the UK. Another post noted that Europe has a greater reliance on public transport.

Meanwhile in 'Chindia' the newly affluent still perceive cars as a luxury and fuel as expensive and will seek to buy economic cars -i.e. there will be more 'Tata Nano' types (with 4 people in) and less Hummer H2s in Mumbai- in addition these societies have not developed the 'Kunstler Wasteful Suburban Sprawl' model of living.

In short, US society has developed an existence that is effectively a highly leveraged 'gamble' on the continuation of cheap energy -an existence that will be strained to breaking point in the coming decades.

As to the pump price, we cannot know the future -Black Swans, Bahktaries phase transitions and all but it will probably fit inside the region to the right of this diagram :o)

Regards, Nick.

P.S. Where can I get hold of a copy of The Model -I would love to have a tinker...

Memmel, you did not include federal and state income taxes. In 2007 for a single person without dependents:

Social Security & Medicare: $24,960 * .0765 = $1,909

Taxable income: $24,960 - $5,350 (standard deduction) - $3,400 (1 personal exemption) = $16,210

Federal tax from 2007 schedule X: $782.50 + ($16,210 - $7,825) .15 = $2,040

Total federal tax: $3,949 / year

State tax varies a bit in different states so assume a rate of 3% to cover income, unemployment and disability tax:

$16,210 * .03 = $486 / year

Total tax: $4,435 / year

Actual monthly take home pay: ($24,960 - $4,435)/12 = $1,710 / month

Your guy only has $1,710 - $1,360 = $350 / month after your subtractions. He is not paying for automobile registration (in Arizona, it is 1% of the list price of the vehicle decreasing 10% per year since its model year), repairs nor maintenance. Your guy likely has a used car. He is likely renting a room in a house or has a roommate in an apartment. The utilities and services bill could be significantly different than $260 / month depending upon where he lives and because it is shared with the roommate. In California at the beach the weather is mild, but in Minnesota it is cold in the winter making home heating expenses larger. It is difficult to generalize.

When the economy goes into recession, the investment income of his automobile insurance company will go negative. In 2002 my rate was jacked up 26% in a 6 month period for this reason. After several years it dropped back after their investment income was restored. His utility and services bill will also rise with increasing gasoline price. His landlord will increase his rent to compensate for his increasing expenses. He will be hit with price increases from multiple sources. If possible, he will probably sacrifice the cable and telephone service before the car. He may seek lower rent somewhere else or an extra roommate. He may get a second job, but that is unlikely during a recession. He may supplement his income with blood donation (the blood is donated but the person is paid for his time). If he loses his job, he may sacrifice the apartment to live in the car because it can serve as both transportation and room. An unemployment check paying 50% of his wage can not sustain the apartment, utilities, services and food, but it can pay for food and the car. The car is more important than rent but less important than a mortgage. Becoming unemployed greatly reduces the amount of travel.

Memmel's approach is fabulous. It is great to see it spelled out this way.

I think Memmel underestimates the cost of credit card debt/payments. Memmel figures $100 per month, but if you owe $10,000 at 25% interest, you have to pay $200 per month just for the interest. There are many people who owe much more than this (now that they can't use their home equity as an ATM machine), and the interest rate rises to 25% very quickly if your credit is bad.

Well see the other comment I was off by 50% in the number of people in the wage group.

And obviously I did not want to get into taxes etc.

As I posted as you go higher up the income ladder the disposable income seems to remain a fairly constant percentage

as more money is devoted to homes cars food etc.

Just real quick it seems like you have this sort of model for the US. This is the price point at which demand destruction becomes a issue.

20k === 5 dollars a gallon

40k === 10 dollars a gallon

80k === 20 dollars a gallon

160k+ never

160k+ group

40 dollars a gallon coupled with percentage of population at this income level ensures they can buy plugin hybrids.

Renewable based fuels are sensible economic destruction (depression) reduces the absolute numbers in this group significantly say by 50%. So incomes over 80k probably can handle a transition with reasonable lifestyle changes

Using 40mpg cars for most trips. Decent plug in hybrids for short trips. Trains etc. The only issue is it does not

make sense to subsidize a extensive road network for this small of a percentage of the population. They can afford to drive anywhere but we cannot afford to build them roads. This group can also compete for the best places to live to lower

energy costs etc.

A lot of the 80k group can also transition fairly well.

With 26% of the population making greater than 75k and assuming that half of these get wiped out in a serious economic contraction leaves 15% of the population able to purchase oil at insane prices 20+ dollars a gallon. We use 25mbpd

So that puts final demand at 3.75 mbd double this to include intrinsic uses such as farming freight etc and you get 8mbd.

So if you take this together with purchasing power I see no reason that we won't maintain a class of fairly affluent people pretty much regardless of the price of oil. We can afford to transition this 15% to a decent post peak lifestyle.

Pretty much every single alternative to oil works if you consider you only need to apply them to a demand level 15% of todays levels.

Assume you get 2mbd from Cananda as a fairly constant supply from the oil sands. US production above 2mbpd for some time and CTL + bio resources. And assume that the US controls production in at least Venezuela or Iraq for the foreseeable future and potentially Iran. The US should be able to get sufficient oil supplies to support 8mbd for a long time.